TAAT e-catalog

for

private sector

https://e-catalogs.taat-africa.org/com/technologies/index-based-agricultural-insurance-for-climate-risk-management

Protect farmers’ investment from weather shocks

Index-based crop insurance helps businesses manage financial losses caused by weather conditions such as drought or excess rainfall. It protects farmers by compensating lost production; it shields lenders from the risk of loan default; and can help stabilize supply and repayment for input suppliers and aggregators. Payouts are based on weather or satellite data, or average yields in an agroecological zone, which removes the need for field inspections and reduces operational costs for insurance providers.

This technology is pre-validated.

No formal IP rights

Key points to design your business plan

Index-based insurance can generate revenue by providing financial protection against weather-related losses. A viable business model requires clear definition of how the product is sold, who pays for it, what costs are involved, and how operational risks are managed.

Plan activities around:

The business generates income by selling insurance coverage to farmers and other value chain actors. The product can be delivered through different models depending on the target market:

direct sales to farmers through agents or digital platforms

bundled sales with agricultural credit, where insurance is included in the loan

bundled sales with input packages (seeds, fertilizer) distributed by agrodealers

partnerships with agribusinesses or aggregators who insure their suppliers

Bundled models are often more effective because they reduce farmer liquidity constraints and increase uptake.

Revenue is generated primarily through premium payments. These premiums can be paid:

fully by farmers

partially by farmers and partially by governments or projects (subsidized model)

by financial institutions or agribusinesses covering their clients

Additional revenue can come from:

service fees charged to partners (banks, input suppliers)

commissions from bundled credit or input products

digital platform services supporting enrollment or data management

The main costs to consider include:

data costs: acquisition or access to weather station data or satellite data used to trigger payouts

product design and validation: defining indices, thresholds, and pricing models

distribution costs: agent networks, digital registration systems, partnerships with cooperatives or agrodealers

farmer awareness and training: communication campaigns to explain how the product works

payout costs: compensation paid to farmers when trigger conditions are met

reinsurance: costs of transferring part of the risk to larger insurance providers to manage large-scale shocks

These costs must be balanced with premium revenue to ensure sustainability.

The main customers are:

smallholder farmers exposed to weather risks

farmer groups and cooperatives

financial institutions seeking to reduce loan default risk

agribusinesses that depend on stable supply

Demand is seasonal and occurs mainly before the planting period, when farmers decide whether to invest in inputs. Demand is influenced by affordability, understanding of the product, and trust in the payout system.

Several operational risks affect performance:

basis risk: payouts do not match actual farmer losses, reducing trust and renewal

low uptake: farmers do not enroll due to high cost or lack of understanding

data reliability: inaccurate or insufficient weather or satellite data affects payout accuracy

delivery challenges: weak distribution channels limit farmer access

liquidity risk: large-scale shocks require high payout capacity

These risks can be reduced by improving index design (e.g. using multiple indicators or crop-stage data), ensuring clear communication to farmers, strengthening partnerships for distribution, and using reinsurance to manage large payout events.

For best results, the business model should ensure that the product is affordable, easy to understand, and delivered through trusted partners, while maintaining a balance between premium revenue and operational costs.

| Groups | Positive impacts |

|---|---|

| Women-headed households (poor, high care burden) | Insurance payouts after shocks increase food consumption and stabilize household welfare. |

| Women with direct responsibility for food, health, education expenses | When contracts are aligned to their needs, insurance supports essential household spending and resilience. |

| Members of cooperatives / savings groups (women and men) | Group-based access improves understanding, uptake, and effective use of insurance benefits. |

| Pastoralist women and livestock-dependent households | Gender-inclusive contract design increases demand and improves protection of consumption and assets. |

| Youth farmers (women and men) | Insurance can support investment decisions and adoption of improved practices when understood and trusted. |

| Persons with disabilities in rural areas | Index insurance reduces need for physical verification, improving access to compensation mechanisms. |

Climate adaptability: Highly adaptable

Index-based crop insurance is a crucial tool for climate adaptation, especially in regions where climate change threatens agricultural production. By reducing investment risks, insurance enables farmers, seed companies, banks, and agribusinesses to invest in climate adaptation measures. Programs can also bundle insurance with climate-smart technologies and practices, helping to promote their adoption. Moreover, insurance products and arrangements can be tailored to specific contexts and types of climate-related risks, making them highly flexible and adaptable.

Farmer climate change readiness: Significant improvement

Index-based crop insurance is becoming an increasingly important tool for farmers, seed companies, banks, and agribusinesses as climate change heightens the risks of crop losses due to extreme or adverse weather. As growing conditions become more unpredictable, index-based tools can track weather data and provide timely compensation when conditions negatively affect production. These flexible, data-driven approaches will be essential for building climate resilience and preparing food systems for a future of greater uncertainty.

Environmental health: Not verified

Insurance tools do not directly target environmental health, and their overall impact depends on the context and design of the interventions. While insurance can sometimes encourage agricultural intensification that may harm the environment, it can also be paired with complementary measures to promote sustainable practices and environmentally smart intensification, generating positive environmental outcomes.

Soil quality: Not yet estimated

Insurance tools do not explicitly target soil health, and their effects can vary across contexts. While insurance may encourage fertilizer use, which can improve soil health in the short term, it can also lead to over intensification and soil nutrient depletion. Over the long term, insurance should be complemented with additional tools or practices to promote and sustain healthy soils.

Index-based insurance protects farmers against weather risks such as drought or excess rainfall. Before the season starts, the insurance provider and client fix the amount covered by the policy based on the cost of production, the value of insured inputs, or the size of the loan that is insured. This so-called "sum insured" represents the maximum amount the farmer can receive if damage occurs. Farmers or other value chain actors interested in insurance then pay a premium, usually between 5% and 10% (sometimes even up to 25%) of that amount, depending on the crop, location, and level of risk. This premium is not refunded if no insurance payout is made; it is the cost of being protected against weather risk during the season.

Payouts are triggered automatically when a predefined weather or yield threshold is reached, based on rainfall or satellite data, or average yields in the area. If this happens, the insured farmer or entity can receive any amount, usually ranging from 20% to 100% of the amount covered, depending on the severity of the event. If the predefined threshold is not reached, no payout is made.

Such insurance helps farmers recover after climate shocks by providing cash to cover part of the production loss and to prepare for the next season. It can also improve access to credit because lenders face less risk of default when farmers are insured.

Scaling Readiness describes how complete a technology\’s development is and its ability to be scaled. It produces a score that measures a technology\’s readiness along two axes: the level of maturity of the idea itself, and the level to which the technology has been used so far.

Each axis goes from 0 to 9 where 9 is the “ready-to-scale” status. For each technology profile in the e-catalogs we have documented the scaling readiness status from evidence given by the technology providers. The e-catalogs only showcase technologies for which the scaling readiness score is at least 8 for maturity of the idea and 7 for the level of use.

The graph below represents visually the scaling readiness status for this technology, you can see the label of each level by hovering your mouse cursor on the number.

Read more about scaling readiness ›

Uncontrolled environment: validated

Common use by projects NOT connected to technology provider

| Maturity of the idea | Level of use | |||||||||

| 9 | ||||||||||

| 8 | ||||||||||

| 7 | ||||||||||

| 6 | ||||||||||

| 5 | ||||||||||

| 4 | ||||||||||

| 3 | ||||||||||

| 2 | ||||||||||

| 1 | ||||||||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | ||

| Groups | Positive impacts |

|---|---|

| Women-headed households (poor, high care burden) | Insurance payouts after shocks increase food consumption and stabilize household welfare. |

| Women with direct responsibility for food, health, education expenses | When contracts are aligned to their needs, insurance supports essential household spending and resilience. |

| Members of cooperatives / savings groups (women and men) | Group-based access improves understanding, uptake, and effective use of insurance benefits. |

| Pastoralist women and livestock-dependent households | Gender-inclusive contract design increases demand and improves protection of consumption and assets. |

| Youth farmers (women and men) | Insurance can support investment decisions and adoption of improved practices when understood and trusted. |

| Persons with disabilities in rural areas | Index insurance reduces need for physical verification, improving access to compensation mechanisms. |

| Groups | Unintended impacts | Mitigation measures |

|---|---|---|

| Poor households (women and men) | Payment of premiums reduces food consumption in seasons without payouts (liquidity pressure). | Introduce flexible payment (installments), targeted subsidies, and link with savings groups. |

| Women in male-headed households | Insurance payouts may be controlled by men, limiting impact on women’s welfare. | Register contracts in women’s names, ensure payments to personal mobile accounts, promote co-subscription. |

| Women excluded by eligibility criteria (no land title, no ID, no phone) | Structural exclusion from insurance access. | Use alternative eligibility (GPS, cooperative validation), group policies, assisted enrollment channels. |

| Low-literacy users (especially women) | Misunderstanding of product reduces trust and uptake. | Use visual/audio tools, local facilitators, simple messaging, repeated awareness campaigns. |

| Mobile or remote populations (pastoralists) | Difficulty understanding triggers and accessing services. | Adapt products to mobility patterns, use local agents and flexible communication channels. |

| Better-off farmers (often men) | Capture a larger share of benefits when subsidies are not targeted. | Apply pro-poor targeting, subsidy caps, and monitor benefit distribution. |

| Groups | Adoption barriers | Mitigation measures |

|---|---|---|

| Women-headed poor households | Low liquidity, limited ability to pay premiums, low financial literacy. | Micro-payments, savings-linked insurance, simplified products, targeted training. |

| Women in male-headed households | Limited decision power, time constraints, restricted mobility. | Flexible enrollment (time/location), female agents, safe spaces for engagement. |

| Women without land titles | Ineligibility due to formal requirements. | Use use-right validation, cooperative-based enrollment, alternative KYC systems. |

| Youth farmers | Low experience, irregular income, weak trust in financial products. | Digital + human support channels, simple onboarding, pilot-based trust building. |

| Persons with disabilities | Physical and informational access barriers. | Accessible formats (audio, large text), trained agents, partnerships with OPDs. |

| Rural poor (men and women) | Low awareness, weak distribution channels, low financial literacy. | Multi-channel awareness campaigns, local ambassadors, combined physical + digital delivery. |

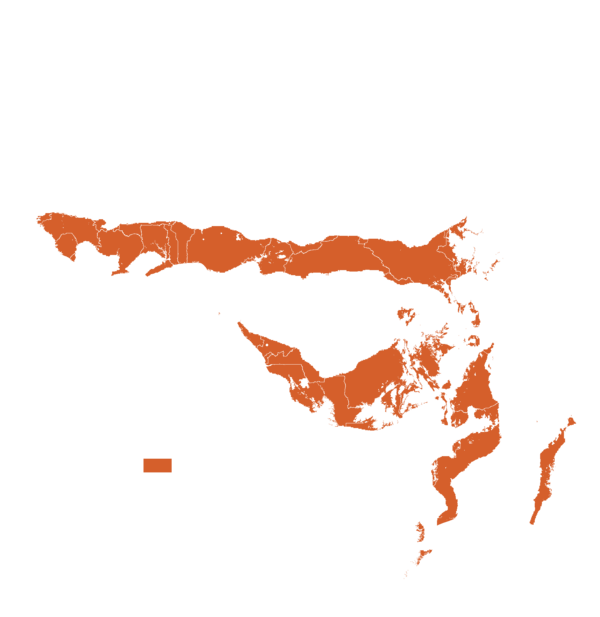

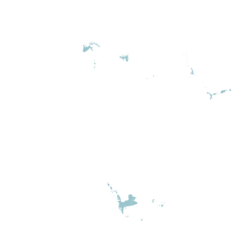

| Country | Testing ongoing | Tested | Adopted |

|---|---|---|---|

| Algeria | –No ongoing testing | Tested | –Not adopted |

| Angola | –No ongoing testing | –Not tested | Adopted |

| Benin | –No ongoing testing | –Not tested | Adopted |

| Botswana | –No ongoing testing | –Not tested | Adopted |

| Burkina Faso | –No ongoing testing | –Not tested | Adopted |

| Burundi | –No ongoing testing | –Not tested | Adopted |

| Cameroon | –No ongoing testing | Tested | –Not adopted |

| Côte d’Ivoire | –No ongoing testing | –Not tested | Adopted |

| Democratic Republic of the Congo | –No ongoing testing | –Not tested | Adopted |

| Djibouti | –No ongoing testing | –Not tested | Adopted |

| Egypt | –No ongoing testing | Tested | –Not adopted |

| Ethiopia | –No ongoing testing | –Not tested | Adopted |

| Gambia | –No ongoing testing | Tested | –Not adopted |

| Ghana | –No ongoing testing | –Not tested | Adopted |

| Guinea | –No ongoing testing | –Not tested | Adopted |

| Kenya | –No ongoing testing | –Not tested | Adopted |

| Lesotho | –No ongoing testing | Tested | –Not adopted |

| Madagascar | –No ongoing testing | –Not tested | Adopted |

| Malawi | –No ongoing testing | –Not tested | Adopted |

| Mali | –No ongoing testing | Tested | –Not adopted |

| Mauritania | –No ongoing testing | Tested | –Not adopted |

| Mauritius | –No ongoing testing | –Not tested | Adopted |

| Morocco | –No ongoing testing | Tested | –Not adopted |

| Namibia | –No ongoing testing | –Not tested | Adopted |

| Niger | –No ongoing testing | Tested | –Not adopted |

| Nigeria | –No ongoing testing | –Not tested | Adopted |

| Rwanda | –No ongoing testing | –Not tested | Adopted |

| Senegal | –No ongoing testing | –Not tested | Adopted |

| Sierra Leone | –No ongoing testing | Tested | –Not adopted |

| South Africa | –No ongoing testing | –Not tested | Adopted |

| Sudan | –No ongoing testing | Tested | –Not adopted |

| Tanzania | –No ongoing testing | –Not tested | Adopted |

| Togo | –No ongoing testing | –Not tested | Adopted |

| Tunisia | –No ongoing testing | Tested | –Not adopted |

| Uganda | –No ongoing testing | Tested | –Not adopted |

| Zambia | –No ongoing testing | –Not tested | Adopted |

| Zimbabwe | –No ongoing testing | Tested | –Not adopted |

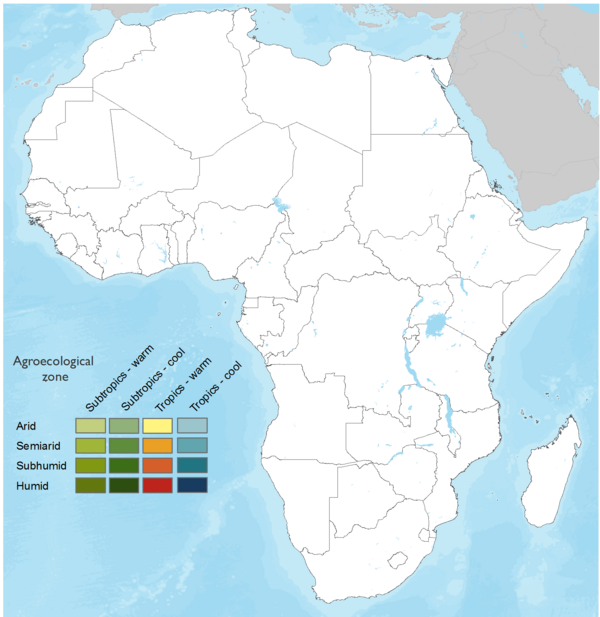

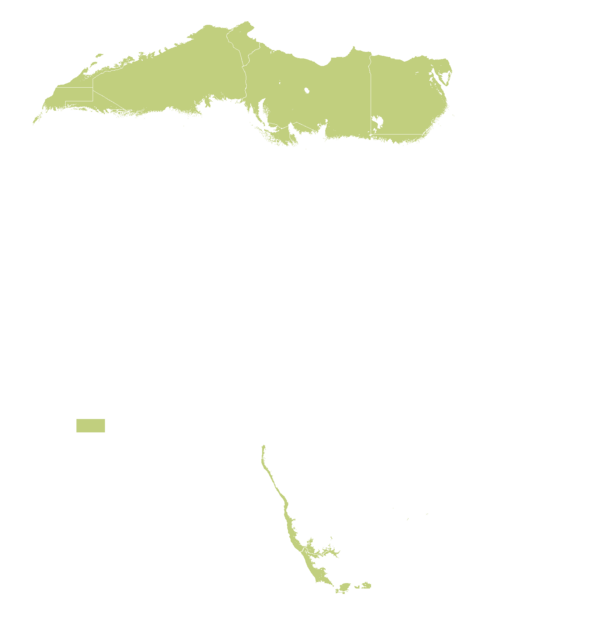

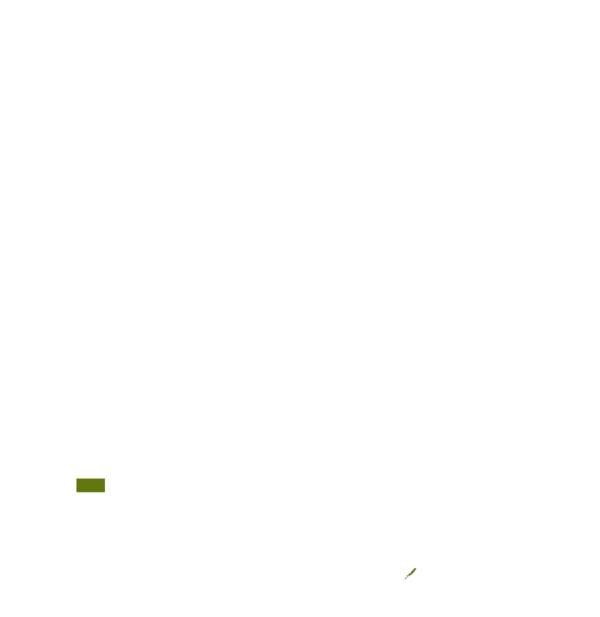

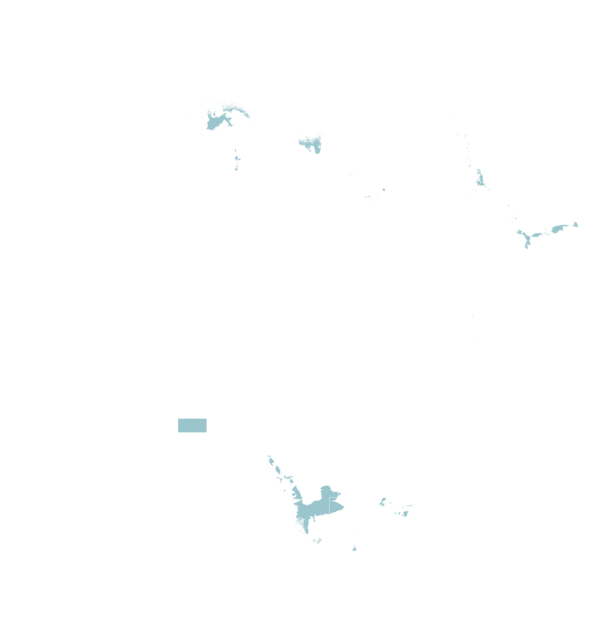

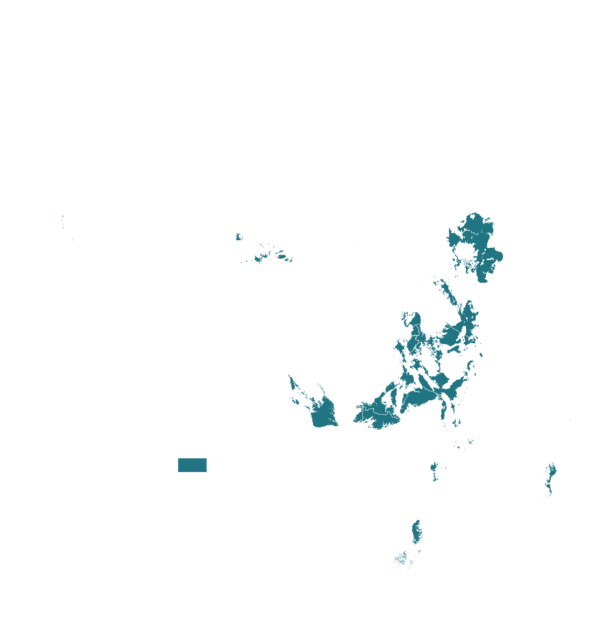

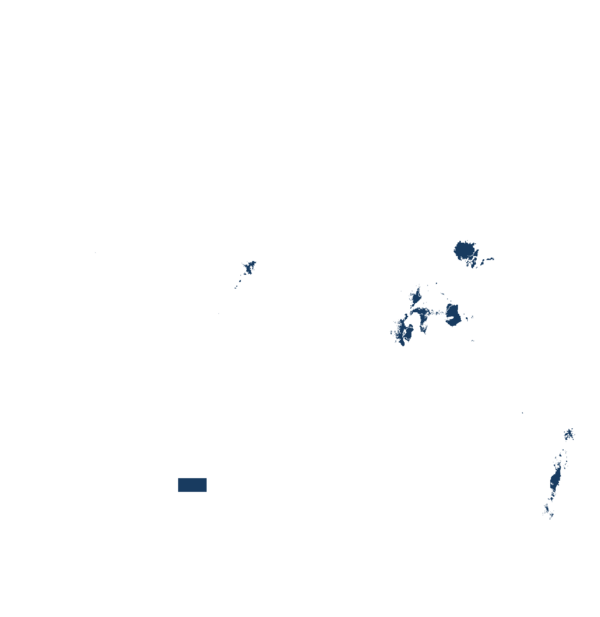

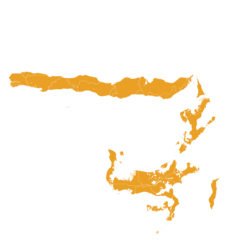

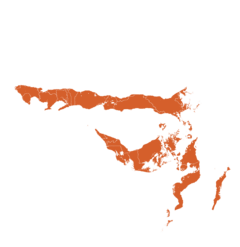

This technology can be used in the colored agro-ecological zones. Any zones shown in white are not suitable for this technology.

| AEZ | Subtropic - warm | Subtropic - cool | Tropic - warm | Tropic - cool |

|---|---|---|---|---|

| Arid | – | |||

| Semiarid | ||||

| Subhumid | ||||

| Humid |

Source: HarvestChoice/IFPRI 2009

The United Nations Sustainable Development Goals that are applicable to this technology.

By protecting food system actors from shocks and enabling investment, index-based insurance can contribute to increased productivity and safeguard incomes.

Index-based crop insurance protects food system actors from unexpected shocks that may impact crop production. By offering payouts when these shocks occur, insurance can protect incomes and make food supply more resilient. Index-based crop insurance also enables investment that can lead to greater productivity and resilience in value chains.

Women are often disproportionately affected by adverse shocks in agrifood systems and therefore stand to benefit significantly from index-based crop insurance.

Index-based crop insurance protects the livelihoods of food system actors from external shocks. Insurance payouts can help actors recover faster after a shock and avoid selling off productive assets. Insurance also enables investment that can improve livelihoods by increasing productivity and resilience.

Index-based crop insurance offers a safety net for low-income food system actors who are particularly vulnerable to shocks. By providing payouts when shocks occur, insurance can help them avoid selling off assets and falling into a poverty trap.

Index-based crop insurance is a critical tool for climate resilience in food systems that can allow food system actors to cope with increased uncertainty and risk driven by more frequent extreme weather under climate change.

4. Farm as usual during the season

Continue your normal farming activities. The insurance does not require field inspections or reporting of losses.

5. Follow seasonal updates (if available)

Some providers share updates on rainfall or crop conditions. These can help you understand how the season is progressing.

6. Receive payout if conditions are met

If the measured weather conditions in your area reach the defined threshold, you automatically receive a payout. You do not need to submit a claim.

7. Use the payout to recover

Use the compensation to cover part of your losses, repay loans if needed, and prepare for the next season.

Last updated on Jun 29, 2026

This technology can be used in the colored agro-ecological zones.

Index-Based Agricultural Insurance for Climate Risk Management

https://e-catalogs.taat-africa.org/com/technologies/index-based-agricultural-insurance-for-climate-risk-management

Last updated on 29 June 2026, printed on Jul 26, 2026

Enquiries e-catalogs@taat.africa